Contents

Overview

The concept of debt cancellation has ancient roots, appearing in various forms across civilizations as a means to alleviate economic distress and reset societal balances. In the modern era, formalized loan forgiveness programs gained traction in the United States following the expansion of federal student aid in the mid-20th century. Early programs were often tied to military service or specific professions deemed critical, such as teaching in underserved areas. The Public Service Loan Forgiveness (PSLF) program, established by the Heroes Act of 2007, marked a significant expansion, aiming to forgive remaining federal direct loan debt for borrowers who made 120 qualifying payments while working full-time for government or non-profit organizations. This program, however, became a focal point for criticism due to its complex requirements and low approval rates, leading to subsequent administrative reforms and calls for broader reform.

⚙️ How It Works

Loan forgiveness programs operate by setting specific criteria that borrowers must meet to qualify for debt cancellation. For federal student loans in the U.S., common pathways include income-driven repayment (IDR) plans, where remaining balances are forgiven after 20 or 25 years of payments, and PSLF, which requires 10 years of qualifying payments in public service. Other programs, like those for teachers or nurses, often require a commitment to work in high-need areas for a set period. Private lenders and some employers may also offer forgiveness programs, typically tied to employment longevity or specific achievements. The process generally involves application, verification of employment and payment history, and a final review by the loan servicer or program administrator.

📊 Key Facts & Numbers

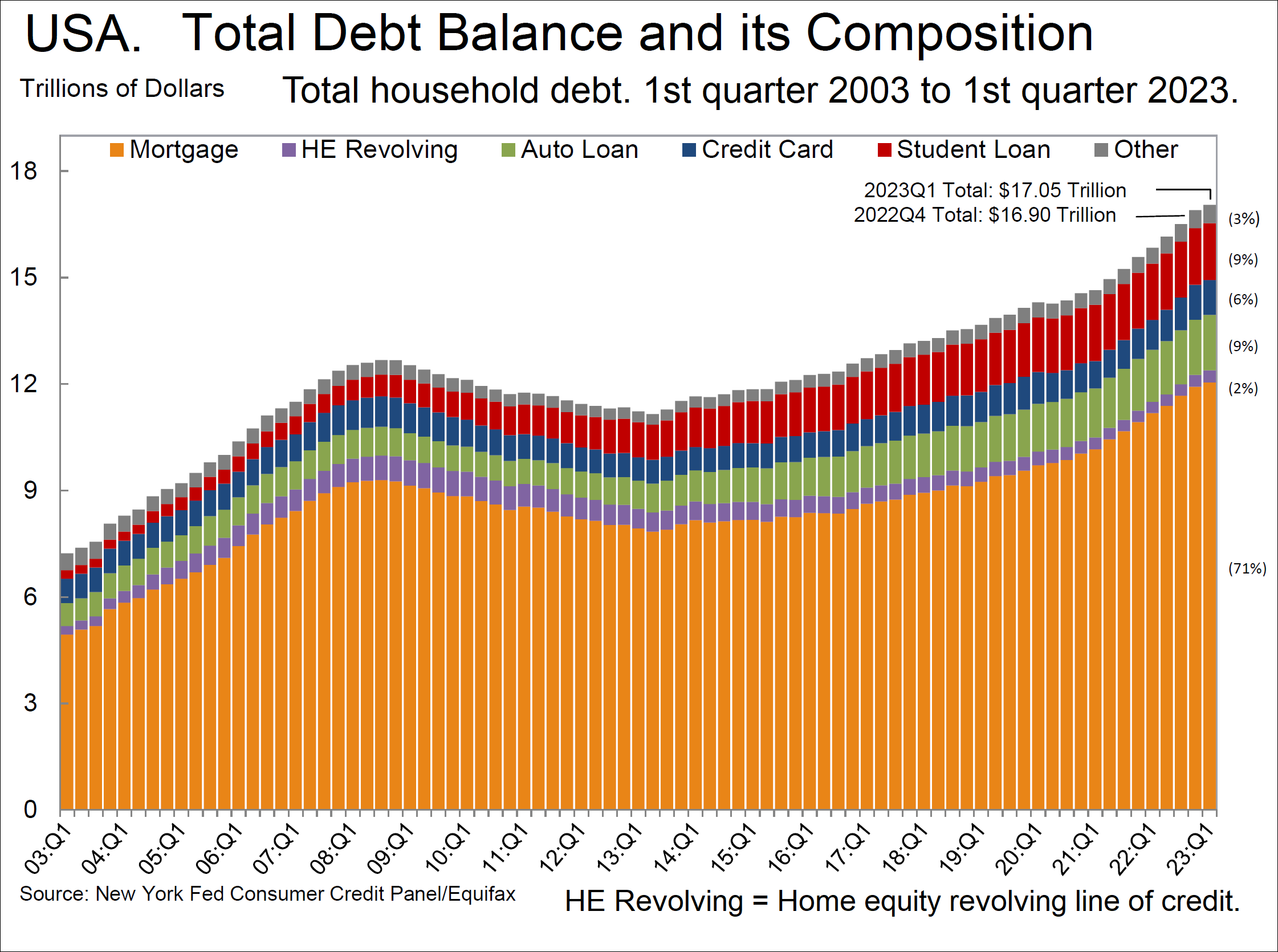

As of July 2021, total student loan debt in the U.S. surpassed $1.73 trillion, with approximately 43 million borrowers holding federal student loans. The average debt for a bachelor's degree recipient in 2019 was around $30,000. The PSLF program, despite its intent, had a historically low approval rate, with fewer than 10% of applicants approved as of late 2021, though this figure improved following administrative waivers. In 2022, President Joe Biden's administration announced a plan for up to $10,000 in federal student loan forgiveness for individuals earning under $125,000 annually, and up to $20,000 for Pell Grant recipients, a move projected to benefit tens of millions of Americans and cost an estimated $300 billion.

👥 Key People & Organizations

Key figures and organizations involved in loan forgiveness include the U.S. Department of Education, which administers federal student loan programs, and various loan servicers like Nelnet and MOHELA. Policy advocates such as the Student Borrower Protection Center and The Institute for College Access & Success (TICAS) play crucial roles in lobbying for reform and assisting borrowers. Politicians like Senator Elizabeth Warren and President Barack Obama have been instrumental in proposing and implementing different forgiveness initiatives. The Consumer Financial Protection Bureau also monitors and regulates loan servicing practices.

🌍 Cultural Impact & Influence

Loan forgiveness programs have a profound cultural impact, particularly in the United States, where student debt has become a significant economic and social burden. For many, the prospect of forgiveness offers a lifeline, enabling them to pursue homeownership, start families, or invest in businesses. Conversely, the perceived inequities and complexities of these programs can foster resentment and distrust in the financial system. The debate over forgiveness also highlights broader societal discussions about the value of higher education, the role of government in managing debt, and the fairness of economic opportunity. The cultural narrative around student debt has shifted from one of personal responsibility to a recognized systemic issue, influencing political discourse and voter priorities.

⚡ Current State & Latest Developments

Recent developments in loan forgiveness have been dominated by the Biden administration's efforts to address the student debt crisis. Following the widespread implementation of waivers and fixes to the PSLF program, which significantly increased approval rates in 2022, the administration moved forward with its broader targeted debt relief plan. This plan, announced in August 2022, aims to provide substantial relief to millions of borrowers. However, the legality and implementation of this broad forgiveness plan faced immediate legal challenges, with a case reaching the Supreme Court. Meanwhile, ongoing efforts continue to streamline IDR plans and address issues with loan servicing that have historically hindered borrower access to forgiveness.

🤔 Controversies & Debates

The controversies surrounding loan forgiveness programs are multifaceted. Critics argue that broad forgiveness is regressive, disproportionately benefiting higher earners, and that it could exacerbate inflation and encourage future over-borrowing. Concerns are also raised about the immense cost to taxpayers, estimated in the hundreds of billions of dollars for large-scale relief. Furthermore, the complexity of existing programs like PSLF has led to widespread confusion and frustration among borrowers, with many being denied despite believing they qualified. Debates also center on whether forgiveness addresses the root cause of high tuition costs or simply acts as a temporary fix. Some argue that alternative solutions, such as tuition-free college or more robust income-based repayment systems, would be more equitable and sustainable.

🔮 Future Outlook & Predictions

The future of loan forgiveness is uncertain, heavily dependent on legal rulings, political will, and evolving economic conditions. Potential outcomes range from the full implementation of broad forgiveness plans to more targeted, incremental reforms. Experts predict a continued focus on streamlining existing programs and potentially creating new pathways for relief, especially for those in public service or facing severe financial hardship. There's also speculation about the role of private lenders and employers in offering more innovative forgiveness solutions. The long-term impact on higher education financing and the overall student debt landscape remains a critical question, with potential shifts towards more affordable education models or increased reliance on income-share agreements.

💡 Practical Applications

Loan forgiveness programs have direct practical applications for millions of individuals and professionals. For instance, a teacher working in a low-income school district might qualify for Teacher Loan Forgiveness, allowing them to have a portion of their federal student loans discharged after five years of service. Similarly, a doctor agreeing to work in a rural health clinic could benefit from the National Health Service Corps Loan Repayment Program. Small business owners who received Paycheck Protection Program (PPP) loans during the COVID-19 pandemic could have those loans forgiven if they met specific employee retention and fund usage criteria. These programs are designed to incentivize specific behaviors and career choices by mitigating the financial burden of debt.

Key Facts

- Category

- finance

- Type

- concept